Pulling the Plug...

Pulling the Plug...

The Federal Reserve's emergency liquidity measures come into focus as tightening of financial conditions begins to head toward a terminal outcome

The King is Dead…Long Live the King (Part Deux):

In our last issue (The King is Dead…Long Live the King - July 28, 2022), we noted that, despite the calls of many for dollar debasement (from global inflation), as the Federal Reserve continued tightening financial conditions global markets would begin to suffer the effects of a stronger dollar. Specifically, we noted:

The US Dollar: Continued strength in the US dollar posed a continued threat to risk-assets. While any weakness in the US dollar had the potential to give risk-assets a bid.

Short End Rates: The Federal Reserve was still engaged in the process of tightening financial conditions in an effort to rein in inflation and short end rates would begin to price a terminal price (i.e. a price at which no further hikes were expected). Further, given the terminal price (at the time) was below the Federal Reserve’s guidance, it seemed likely the terminal price assessed by the futures market (and the duration for which the terminal price would be held before cuts) was too low. To cause the futures/forwards curves to reprice terminal at a higher level, we noted the Federal Reserve might seek to use their “dot-plot” or “Summary of Economic Projections” (SEP) to dictate expectations of future hikes and the length of time for which those hikes would be maintained. We noted that, as a result, after the upcoming Fed meetings (that occurred in August/September), forward swap curves/futures would likely more restrictively price a higher terminal rate. After that point any subsequent decrease in the pace or magnitude of hikes would likely be seen as “relief” from tightening.

Long End Rates: A meaningful drawdown in Federal Reserve Balance Sheet Assets from QT had yet to occur (but was imminent). We also noted that as this process began, it could have a significant impact on treasury liquidity (and long-end prices), i.e. rates might rise on the long-end and long duration assets may suffer. We also noted that (1) long-end rates are sensitive to growth prospects and would be balancing out the prospects of pricing in a growth recession as well, and (2) the Federal Reserve might seek to modulate the impact on treasury liquidity using regulatory relief.

Credit Spreads, Housing Activity and Mortgages: Further deterioration in credit seemed likely as the Federal Reserve continued on its tightening path. HY spreads would likely continue to widen and HY issuance would also likely slow down significantly. Similarly, MBS and housing activity seemed likely to experience continued weakness as the Federal Reserve continued tightening.

Unemployment: While the inflation fight was center-stage, there was/is a point at which the unemployment rate becomes relevant and would emerge as an important indicator for the Federal Reserve in determining their tightening regime.

Regulatory/SLR Relief: The Federal Reserve was/is sitting on certain liquidity facilities and regulatory tools that the Fed might use in an attempt to soften the economic landing of tightening (most notably the “supplemental leverage ratio” (SLR)).

Rates Volatility: As recession (more accurately “recession fears”) caused the dollar (and long-end rates) to reprice (i.e. fall), this would have the simultaneous effect of loosening financial conditions (i.e. easing the effects of the “dollar wrecking ball”). Loosening financial conditions into an inflationary environment causes inflation expectations to rise, which would thus, put the Federal Reserve in danger of a “stop-go” feedback mechanism the Fed would most likely (and should be) eager to avoid.

Distress in Emerging Markets/Europe/Japan: As the Federal Reserve tightened monetary policy, all countries with large US dollar needs (nearly all of the world) would tighten involuntarily as well. Deleterious effects of Federal Reserve tightening in these nations would cause pressure in the FX markets. We also noted that this “dollar wrecking ball” is sometimes associated with a “credit event” and tends to negatively impact earnings globally (until ultimately the effect on growth is so severe that the strength of the dollar begins to fail of its own strength).

Energy Crisis: Simultaneous with dollar strength, an energy crisis had emerged (particularly focused in Europe and other nations wedged between the BRIC, physical/commodity producing world, and the debt-financialization Anglosphere).

As the months have progressed, we have seen these 9 observations unfold in real-time:

First, since our last edition on July 28th, the US dollar has appreciated dramatically. Most notably, the USD paused briefly in the month of August (during which a large relief rally in risk occurred) before reasserting its strength and appreciating >5% as of this writing in October (this was on top of the prior 10% increase from our last edition for a total appreciation of >15%). The subsequent strengthening of the dollar was a headwind for risk, causing risk assets (over the same period) to retrace any gains they experienced during the month of August (and to end largely unchanged for the period).

Second, as the US dollar weakened in the month of August (and inflation expectations began to pick up once more), the Federal Reserve (most notably at Jerome Powell’s Jackson Hole press conference) recommitted to its tightening stance. In September, the Federal Reserve followed up on this commitment by communicating a more aggressive “higher for longer” assessment of its “dot plots” via its Summary of Economic Projections (SEP) and a relatively consistent/coordinated communication channel of Federal Reserve governors making statements of “higher for longer” statements on inflation). As a result, the short-end of the Treasury curve (2Y) accelerated dramatically over the period with yields rising >30% (to a yield of ~4.5%).

Third, as quantitative tightening began causing the Balance Sheet to materially decline (as deferred scheduled purchases finally reached their conclusion), the long-end of the treasury curve (10y) responded in kind with yields rising >50% (to a yield of ~4%). Notably treasury market liquidity has also declined considerably over the period (leading many to grow concerned about the Treasury market’s ability to function without some form of relief from the Federal Reserve or US Treasury).

Fourth, despite a brief period of tightening (which coincided with August’s relative dollar weakness and easier liquidity conditions), credit spreads have begun to widen considerably (although they continue to remain below 2020 COVID highs). Similarly, on the back of accelerating long-end yields, mortgage rates have hit multi-decade highs of >7% (30-year fixed rate). This has caused housing affordability to decline considerably (to one of the worst levels in >30 years) and housing activity to materially slow as a result.

Fifth, unemployment has remained remarkably resilient throughout the period, evidenced most notably by the fact, the unemployment actually declined (rather than increased as desired by the Fed) to 3.5% (down from 3.7%). While a declining unemployment rate is normally positive news, in the context of a fight against structurally higher inflation, the Federal Reserve has actually inadvertently moved away from it’s goal of fighting wage inflation. Presumably, in reaction to this, Federal Reserve messaging has become more explicit over the period that an unemployment rate as high as 4.5% will be considered “acceptable” to prevent wage inflation from intrenching. Anecdotally, it should also be noted that over the period, a number of labor unions have organized demanding higher wages (which is contrary to the Federal Reserve’s goals of preventing a “wage-price spiral”) among major corporations (Amazon, Starbucks and Lowe’s among others: US News: Labor Organizing and Strikes).

Sixth, while the Federal Reserve has not made any efforts to employ regulatory relief as of our last writing, its notable that chatter in the space has picked up considerably. Most notably, CEO of JP Morgan, Jamie Dimon, more or less stated his request specifically for regulatory relief in a nearly explicit exchange for having his bank participate intermediating the increasingly illiquid Treasury market. (JPMorgan, Citigroup say higher capital requirements may hurt...)

Seventh, after financial conditions loosened in August on the mere anticipation of a slightly less aggressive policy stance by the Federal Reserve (which quickly gave way to “pause” or “pivot” talk among market participants), Federal Reserve Chairman Jerome Powell doubled-down on the Federal Reserve’s inflation fighting stance in a short, rather terse, statement at the Federal Reserve’s annual Jackson Hole symposium. (“The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.”) In later weeks, on renewed pivot talk among market participants, Federal Reserve governors have explicitly stated the need to maintain tight policy in the face of economic, even in the face of economic weakness, to prevent having to resort to the ‘stop-go’ policy of the ‘70s.

Eighth, emerging markets, the Eurozone and Asia-Pacific have endured significant stress on the back of the US dollar’s historic appreciation. In an unusual move, both the IMF and the UN made public announcements imploring the Federal Reserve to end their tightening cycle or force emerging markets to suffer severe consequences (U.N. Calls on Fed, Other Central Banks to Halt Interest Rate Increases). In Asia-Pacific, both Japan’s and Australia’s currencies have begun to significantly depreciate against the USD. This is most notable in Japan, where continuous efforts to support the bond market began causing such currency distress that FX interventions were employed. Despite these FX interventions, USDJPY continued to push through the 150 level. Australia also notably decreased the pace of their hiking/tightening cycle out of step with the Federal Reserve (presumably in a nod to their housing market which is funded in large part by floating rate mortgages). Canada, which has similar housing woes to Australia, has also similarly fallen out of step with the Federal Reserve’s hiking cycle. In the Eurozone, both the Euro and the British Pound fell to parity against the USD. Notably, in the UK (formerly a part of the Eurozone, but now Brexit’ed), a liquidity crisis ensued (in the form of a pension crisis), when embedded leverage in structured products (called “LDIs”) held on pension balance sheets triggered an uncontrolled sell-off in “Gilts” (10-year UK government debt), leading the Bank of England to step in and support the Gilt market in a “temporary” bond purchasing program (to prevent a liquidity crisis and collapse of it’s sovereign debt) (BoE to start selling bonds...but no longer long-dated Gilts). This intervention temporarily relieved pressure in the British pound and the Euro, (although pressure may return if/when these operations cease). It should be noted that globally, pensions (and insurance companies) use similar structured products to boost return that makes them vulnerable to liquidity crunches and fire sales of assets (pensions and insurance; historically were extremely liquid institutions and as such regulations focus almost entirely on “solvency” issues, but not “liquidity” issues, however, post-GFC many of these institutions have allocated increasingly to illiquid assets/alternatives, structured products and derivatives to boost returns in a world starved of yield and are now subject to collateral calls and margin requirements that regulators have not fully stress-tested). In a nod to “Triffin’s Dilemma”, the Federal Reserve seems to have largely taken the position that “It’s not the Fed’s responsibility to tackle the issues of other countries” (attributed to Federal Reserve Governor Waller).

Ninth, after a significant reduction in oil prices (owing in part to the US government’s release of oil from the Strategic Petroleum Reserve), the BRIC nations (mainly via OPEC+) opted to reduce the supply of oil to the marketplace (despite already tight supply) to further support elevated oil prices. This act exacerbates pressure on headline inflation, like food (which use oil as a critical input cost).

Pulling the Plug…

“I fully expect that there are going to be some losses and there are going to be some failures around the global economy as we transition to a higher interest rate environment, and that’s the nature of capitalism…It should not be up to the Federal Reserve or the American taxpayer to bail people out.” – Federal Reserve Governor Neel Kashkari (Kashkari says Fed is quite a ways away from pausing rate hikes)

As financial stability risks have inevitably arisen from rates volatility, the Federal Reserve has found itself caught between it’s three mandates (more thoroughly discussed in “The Beatings Will Continue Until Morale Improves - April 28, 2022), inflation, financial stability, and unemployment.

As an initial matter, the unemployment mandate has completely fallen away in the face of inflation. That is to say, the mandate is now actually to cause unemployment (up to an acceptable maximum as determined necessary by the Fed to quell wage inflation) rather than to minimize it. Which leaves the conflicting mandates of fighting inflation by tightening liquidity conditions without causing financial instability.

The financial system, however, has proven incredibly fragile (perhaps no surprise, given more than a decade of financial “morphine” being delivered in steady doses). A ~20% drawdown in equities and a ~50% move in long-end yields has been sufficient to cause a liquidity event in UK sovereign debt (via it’s over leveraged pension system). This presents a serious conundrum for the Fed as it stands in a position where the financial markets are teetering on the brink of collapse (the eagerness for a Fed pivot being palpable among market participants who are desperate for what most feel is the inevitable return of the magical QE elixir) and yet, no meaningful progress has been made on services or wage inflation, as noted above the unemployment rate has actually decreased during the tightening process (although goods inflation has moderated and housing appears to be in early stages of rolling over, demand overall is still well above trend as evidenced by the fact real GDP was positive for the period and nominal GDP continues to run roughly double, at ~6%, the long-run trend of ~3%). This presents a very serious (and dangerous) picture for market participants, one in which the Fed is almost certainly going to have to permit some market failures. The problem is in fact so pervasive, that at least one Federal Reserve Governor (Neel Kashkari) has stated it openly, essentially stating, “yes, things are going to fail, it’s not our job”.

…but keep the Defibrillator Close By

Notably, however, this statement is made in the context of a Federal Reserve which has spent the better part of the three years since the COVID-19 collapse of the Treasury market (and associated bond markets) building a series of liquidity facilities and regulatory buffers to employ in the event of funding market distress. These are more fully discussed in our issue “Structural Changes in Treasury Market Suggests Policy Shift” from more than a year ago (September 1, 2021). But we will revisit some of the more salient ones likely to be employed below for emphasis.

1) Foreign Liquidity Facilities

a. FX Swap Lines: FX Swap lines are a currency exchange set up between central banks such that should a central bank find their USD reserves running low, they could exchange their own currency for USD directly from the Federal Reserve.

b. Foreign and International Monetary Authorities (FIMA) Repo Facility: This facility functions as a repurchase program whereby a foreign Central Bank can pledge US Treasuries from their reserves to the Federal Reserve and receive USD in exchange.

The combined effect of these two facilities should be to minimize foreign dollar funding stress should it arise (it also has the domestic purpose of preventing a run on US dollars which could result in forced selling of US treasuries out of foreign central bank reserves).

2) US Domestic Liquidity Facilities & Potential Operations

a. Reverse Repo Facility (RRP): Money market funds “lend” (aka deposit) cash at the Fed and the Fed posts collateral of a Treasury plus interest (practically the Fed doesn’t post the collateral they just pay interest to the money market fund at the stated rate). This tool ensures that money market funds don’t bid down Treasury bill yields lower than the Effective Federal Funds rate (e.g. the interbank lending rate) through which the Fed transmits tightening policy. It essentially serves as Interest on Excess Reserves (IOER) for money market funds. That is to say, it provides a floor on the policy rate by allowing non-banks a place to park their excess cash at the Fed outside of the treasury market (thereby avoiding a “collateral shortage” or shortage of Treasury bills that might drive rates down when the Fed is trying to raise rates). Interestingly, the converse is also true. Because this excess money market fund cash is just sitting at the Fed (~2T at last check) and the Fed controls the policy rate as well as the issuance rate of Treasury bills, the Federal Reserve has some level of “control” over this liquidity. Or said another way, by altering the economic returns of the RRP rate vs. the T-bill rate, the Fed can flush this cash into the treasury market to flood it with liquidity should the need arise.

b. US Treasury Buyback Program: Logically, using the RRP as a liquidity buffer sounds fine in theory, but would seemingly only work for providing liquidity to T-bills (i.e. the short-end of the yield curve). What happens if Treasury illiquidity occurs in the long-end (which it tends to since the 10-year treasury is one of the most common forms of collateral globally)?

The US Treasury (as the issuer of US debt) has the ability to repurchase US Treasuries from the open market (effectively cancelling the debt by prepaying). The US Treasury also has the ability to issue new debt at varying maturities (provided it loosely falls within an average duration profile that is suitable to fund the US government over the long term). That is to say, the US Treasury has the ability to “twist” the curve, by purchasing long-end treasuries while issuing short-end treasuries in roughly equivalent amounts. This shortens the average duration of the total US government debt, but resolves any liquidity shortage in the long-end by pushing cash from RRP to T-bills to T-notes; thereby giving the Federal Reserve (in coordination with the US Treasury) some control over the liquidity profile of the US Treasury market in its entirety (its estimated they can support this operation up to roughly 3T, which perhaps more than coincidentally, roughly correlates to the total liquidity available in RRP).

c. Standing Repo Facility (SRF): US Treasuries can be posted as collateral to the Fed in exchange for US dollars. This protects the US repo markets against a run on US dollars (typically by US banking institutions), by allowing institutions to transact directly with the Federal Reserve if other banking institutions refuse to transact with them (for fear of counterparty risk or other reasons). The Federal Reserve currently maintains a ~600B cap on this facility (but it seems likely this could be increased if needed, since Congress seemingly wouldn’t object to avoiding a US bank run on US dollars).

The combined effect of these domestic facilities are that the Federal reserve should be able to prevent a collateral shortage on one side (too much cash not enough USTs as we are currently experiencing) via the RRP and a dollar shortage (too many USTs not enough cash as was experienced during the COVID-19 crisis) via the SRF. Essentially, the domestic repo market now has bumpers like a bowling alley to prevent runs on collateral (USTs) and runs on dollars (USD) on either end and if the treasury curve doesn’t behave between the bumpers, the US Treasury Department can twist the curve by shifting its duration profile via buybacks and issuance as needed.

If the Fed determines the treasury market requires additional liquidity (beyond what they are prepared to supply themselves via their various facilities), they can also release some out of regulated financial institutions (i.e. banks) by granting them regulatory relief from the supplemental leverage ratio (SLR) as discussed in last issue (The King is Dead…Long Live the King – April 28, 2022). That is to say, because certain regulatory restrictions on bank capital are not risk-adjusted, banks decline to participate in making markets in areas where doing so would take up a lot of balance sheet space on their books (in favor of higher profit, less capital intensive activities). Allowing banks to participate in these activities without affecting their regulatory caps would add liquidity to the marketplace, most notably the treasury market (assuming banks agree to participate).

Interestingly, many market participants noticing the rapid rise in yields and decline in Treasury market liquidity have come to conclude that a bailout is imminent (or that a bailout must be conducted or the financial system will collapse). In many ways, this may be a conditioned behavior from more than a decade of Federal bailouts, where every crisis is met with a public sector solution. It is notable, however, that the Federal Reserve (in coordination with the US Treasury) spent almost 3 years setting up various facilities to allow the private sector to stand on its own once more. It seems highly unlikely the Federal Reserve would opt to simply bailout the entire financial system rather than at a minimum testing the facilities they took painstaking effort to set-up over many years to address systemic funding market stress.

Financial Stability Risks

This is not to say that there are no risk of failures in the financial system. These risks just largely exist outside of the Federal Reserve mandate (and the mandate of global central banks more generally) in a “shadow banking” system that has largely sprung forth (via the securitization chain and complex derivative products) with the express purpose of funding the highly leveraged activities, the restrictive Dodd-Frank/Basel III regulations were designed to prevent global financial institutions from partaking in directly. The UK pension/sovereign debt liquidity crisis is a harbinger for the rest of the world (most pensions/insurance use similar structured products and swaps to hedge/boost returns and in many ways operate as poorly run hedge funds rather than true pension or insurance schemes). The open question, however, is if these failures will be permitted by the Federal Reserve (technically speaking any failures that would occur, would occur outside of the Federal Reserve mandate, i.e. outside of US dollar and US Treasury funding markets). Will the Federal Reserve bailout mis-priced corporate credit? Collateralized Loan Obligations? Leveraged Loans? High Yield Debt?

Given the facilities set up by the Fed and their reluctance to use any of them, it seems likely it’s actually the Federal Reserve’s goal to cause a significant drawdown in asset prices (a widening of spreads in credit, a loss of value in equities, etc.). That is to say, if they wanted to flush the system with liquidity today, they could. They have the systems in place. They’re choosing not to (at least so far).

The probable reasons for this are fairly straightforward:

First, after more than a decade where flooding the system with liquidity had no consequence, additional liquidity now has a direct reaction function with inflation expectations. Looser liquidity conditions increase inflation expectations. Increasing inflation expectations, generally speaking, is bad for the Federal Reserve. It’s the institution’s primary societal role to maintain stable pricing. Reducing liquidity conditions decreases inflation expectations. In a fight against inflation, few things are more deflationary than permitting a fair bit of debt to deleverage (since debt is a form of money creation and default is a form of money destruction) and perhaps few things are more self-reinforcing for institutional power than allowing a sector that exists outside of your regulatory mandate (really in many ways in contravention of your regulatory efforts) to deleverage.

Second, mechanically, forcing MMFs out of RRP into T-bills amounts to a short-end rate cut (since it removes the floor under the policy rate as discussed above and creates demand for bills driving the bill price down). Practically speaking then, it doesn’t make mechanical sense for the Fed to raise the policy rate (i.e. raising the Federal Funds Rate) while forcing liquidity out of RRP (and thereby removing the floor under that policy rate), since doing so would be asynchronous. It makes much more mechanical sense for the Fed to wait until they have completed their intended tightening cycle before removing the floor under the policy rate.

Third, the Fed likely wants the market to reprice to a world absent Federal Reserve support. If some things fail along the way, so be it. After living in a financial world of no consequences for more than a decade, there is a lot of proverbial “fat” in the global economy that could use to be trimmed (~20% of S&P companies are “zombies” and unproductive and an elaborate “shadow banking” sector has emerged - outside the watchful eye of the Fed - to take credit risk where regulated institutions post-Basel III/Dodd-Frank cannot). As Mr. Kashari put it, “it should not be up to the Federal Reserve or the American taxpayer to bail people out”. If you can’t pay your debts, you default, that’s capitalism…within a normal distribution of systemic reason.

Despite the forgoing it’s important to note that there is a normal distribution of behavior that is reasonable, i.e. one can go too far the other way by quitting the QE drugs cold turkey. You don’t just take the morphine away from the patient, you will kill the patient. There’s a weaning process.

An uncontrolled deleveraging can create a dangerous asset collapse that would be counter-productive to the Federal Reserve’s efforts to orchestrate a “soft-landing” (and damaging to society generally). It is extremely unlikely the Federal Reserve is going to pop the bubble and stand-back while the whole world burns. It would actually be counter-productive to their efforts to successfully wean the patient off the government provided QE back into a Treasury market that is intermediated by the private sector (albeit now with bumpers on either side of the lanes).

They in fact stand at the ready to intervene. If the treasury market begins to fail for lack of liquidity…CLEAR…hit it with T-bill issuance to drain RRP. If T-note liquidity begins to run dry…CLEAR…hit it with a US Treasury buyback operation. The Fed (in conjunction with the US Treasury) is in a position to jolt the patient back to life as necessary, as the global economy goes through the painful process of walking on its own again.

Counterintuitively, this lack of need/desire to bailout the entire financial system could serve as a trapdoor to risk assets (and the shadow-banking system), most of who’s market participants are conditioned for perpetual bailouts (and an ultimate return to perpetual QE).

The Real Economy

To be clear, these liquidity measures, when deployed will probably set off liquidity impulses. That is to say, if a market is drawing down and the Fed/Treasury suddenly jolt a few trillion dollars into it, markets will rebound. The end destination, however, is still likely lower until prices reach a level that is consistent with the underlying growth of the real economy (and in banking speak a minimum level of excess reserves in the banking system). In the simplest conformation of this process, the Federal Reserve permits a large drawdown in risk assets (widening of credit spreads, etc.) until a perceived breaking point is reached. At this point, liquidity is flushed back into the system (via the relevant facility) which produces a boost to risk and then the deleveraging is permitted to resume until a new crisis arises or the system reaches a stable equilibrium. (You might actually consider this the “softish” landing for financial markets the Federal Reserve governors like to use as a “seed phrase”.)

It should also be noted that this process of deleveraging is a painful one for the real economy. Getting inflation under control requires demand destruction (from the Federal Reserve’s “demand side” perspective), demand destruction means job losses, failed businesses, decreased consumer spending, decreased demand for goods, debt defaults, etc. In financial speak, it means decreased earnings expectations and likely a rather deep recession. It will take the economy time to reach a new state of equilibrium (especially since as a starting point demand is running almost double trendline growth), it will also take markets a fair bit of time to price to this new equilibrium (regardless of volatile swings which may result from hitting credit landmines as liquidity is drawn from the system).

These effects are also exacerbated by structural issues (i.e. oil and food shortages). While the Fed (and US Treasury) spent a great deal of time fortifying funding markets, it is unlikely they fully anticipated or accounted for energy or food crises (or the fiscal responses governments tend to employ to attempt to ameliorate these social conditions). This creates a rather severe wrinkle in the deleveraging scheme central banks around the world are employing, which has the potential to impact the real economy much more severely than most market participants anticipate (as essentially monetary policy - aka the Central Bank’s tightening policies - become incongruous with fiscal policy - aka the government/political desire to alleviate demand destruction by printing more money or providing “economic packages” - Ahead of FOMC Meeting, Chairperson of the US Senate Banking Committee Brown reminds Chair Powell of the Fed's Mandate to Promote Maximum Employment).

While it may perhaps seem like a great deal of time has passed, we are likely still only in the early stages of repricing. That is to say, up to this point, most repricing has been a function of liquidity reduction and resulting multiple compression. A “recession” (whether deep or shallow) has not yet been priced. Ultimately, the severity of damage caused to global growth will determine the ultimate equilibrium price at which the global economy (and therefore asset prices) will reset.

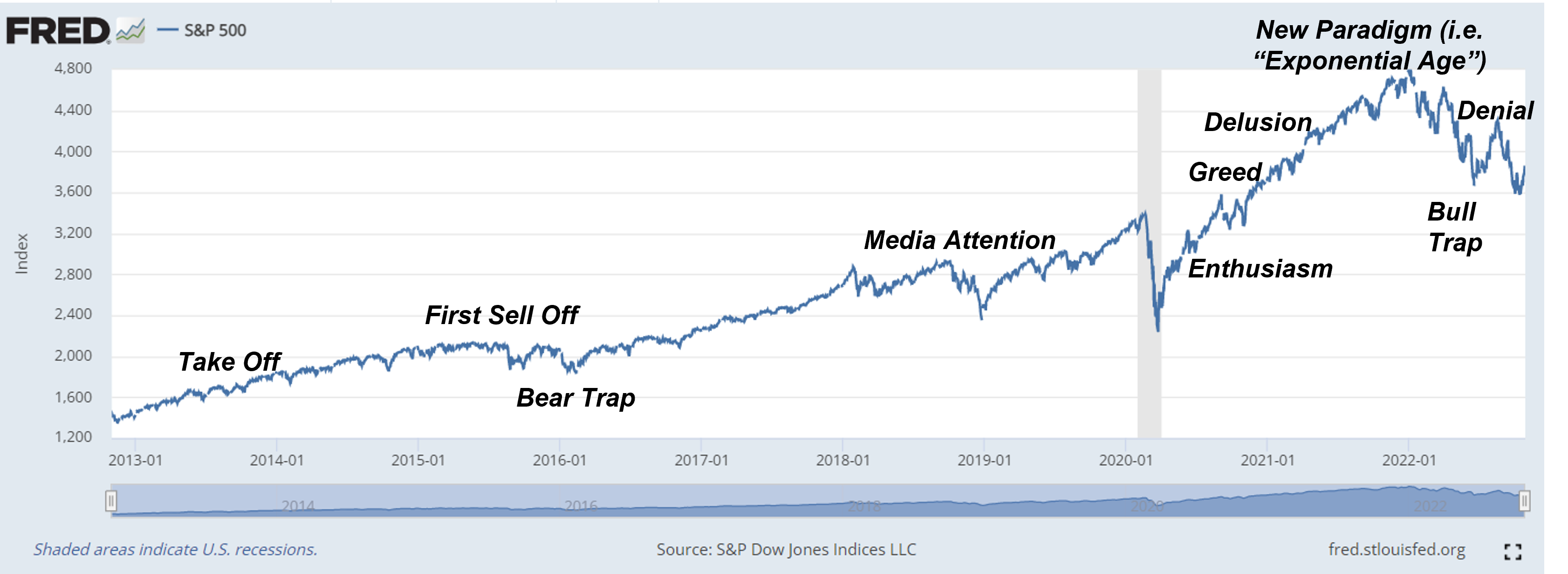

Following on our prototypical bubble chart, we may only be here: at the early “fear” stage.

The observant reader will notice a similar pattern emerging in the S&P500:

Be On The Look-Out:

During this period there are a few important factors to be aware of:

Credit Events Internationally: As we have already seen with the UK pension crisis, the global pension and insurance system contains within hidden embedded leverage that could trigger periodic credit/liquidity crises.

Credit Events Domestically: The US is not immune to credit shocks (particularly in the pension/insurance area and private markets). The US banking system is however more robust than other global economies on a relative basis.

Liquidity Responses by Foreign Central Banks: Look out for signs foreign policy is diverging considerably from US domestic policy as this will exacerbate cross-currency and foreign funding issues. (This is already occurring to some extent in Asia-Pacific and Canada as mentioned above.)

Liquidity Responses by the Federal Reserve/U.S. Treasury: Look out for signs the Federal Reserve (or U.S. Treasury) is preparing to deploy or deploying liquidity apparatuses as this will have a powerful impact on asset prices.

Unemployment Rate: The Federal Reserve is using the Unemployment Rate as a barometer of the relative health/tightness of the labor market. A significant change in the rate of change of unemployment will be a telltale sign that the economy is moving from an inflationary environment into a recession. At this point growth concerns will take over from liquidity/inflation concerns as a recession begins to be priced into the market.

Long-End Rates: As treasury market liquidity continues to dry up rates may rise on the long-end and long duration assets may suffer. Be aware, however, that (1) long-end rates are sensitive to growth prospects and will be balancing out the prospects of pricing in a growth recession as well, and (2) the Federal Reserve may seek to modulate the impact on treasury liquidity using regulatory relief/buybacks. It seems likely that a turn in the unemployment rate would cause the long-end’s attention to shift primarily to growth concerns.

Short-End Rates: As growth begins to roll-over, the short-end of the treasury market will begin to price a recession (this will most likely first be evidenced in the futures/forwards market that will begin to respond). This relative “easing” of financial conditions from this reaction function will be challenging for the Federal Reserve who may very well respond by “overtightening”, i.e. by staying tighter for longer to ensure inflation is under control. This will be damaging to the real economy. Be aware, in particular, of the 2-year treasury. The 2-year treasury will typically invert the 3-month treasury and policy rate (even if the Federal Reserve is holding the policy rate steady) prior to the commencement of a recession (and rate cutting cycle).

Economic Snapshot:

GDP: Q3 $25,663.289 Real GDP growth increased at a rate of 2.6% (up from -0.9% in Q2). Notably, nominal GDP (reported in bold) has continued steadily increasing at a rate roughly double long-term growth trend with the US unemployment rate remaining at historic lows this continues to be indicative of a tight labor market and a generally overheated economy.

Price: Stock market averages continue to remain near all-time highs with the S&P500 closing at 3830.60 on October 26, 2022 (down from 4,023.61 on our last issue on July 27, 2022). Prices remain off the peak and trending down.

Price to GDP: Price to GDP ratios remain historically high with an S&P500 to GDP ratio of 0.1517 (down slightly from our July reading of 0.165, our April reading of 0.1743 and our January reading of 0.1847). Despite these declines, it only has just reached a ratio last seen at the height of the Dot-com bubble.

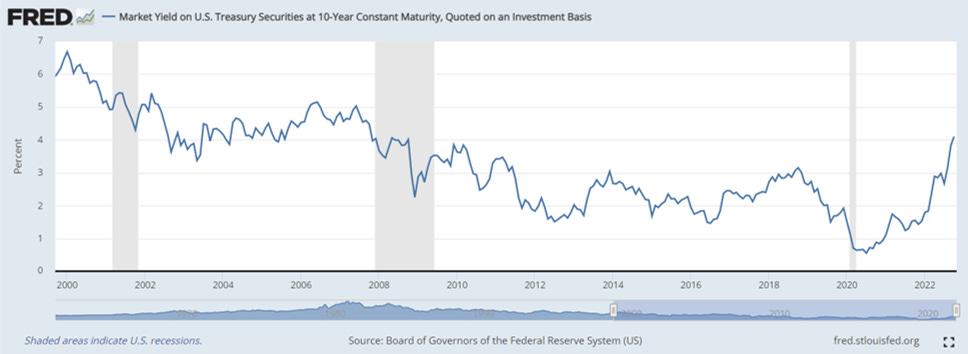

Interest Rates: The 10-Year Treasury Rate rose to has high as 4.1% (up considerably from 2.81% in July 26, 2022).

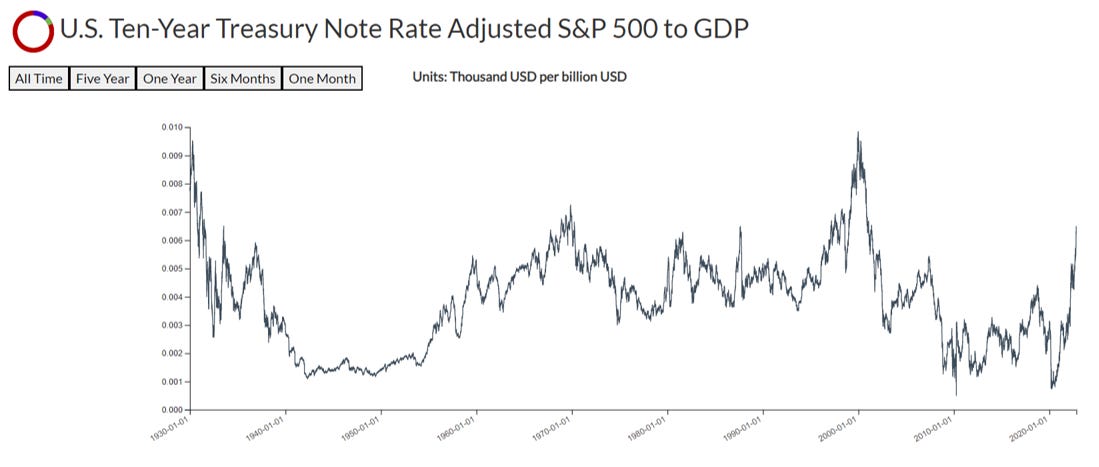

Rate-adjusted Price to GDP: Rate-adjusted price to GDP has accelerated notably since our July reading and now sits at levels last seen in the late 1930s and 1970s (above 2008 levels but still below 2000 levels).

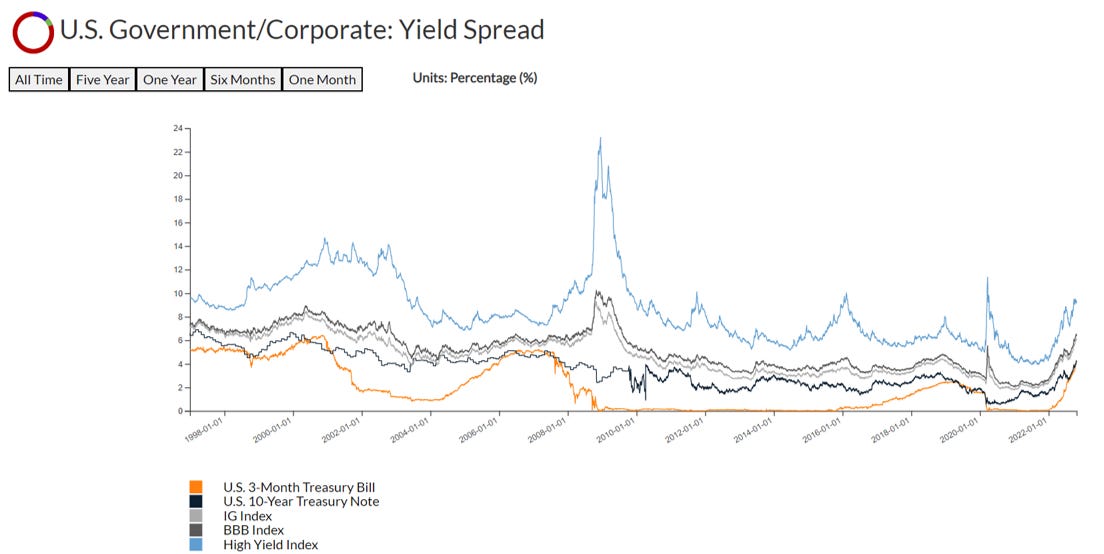

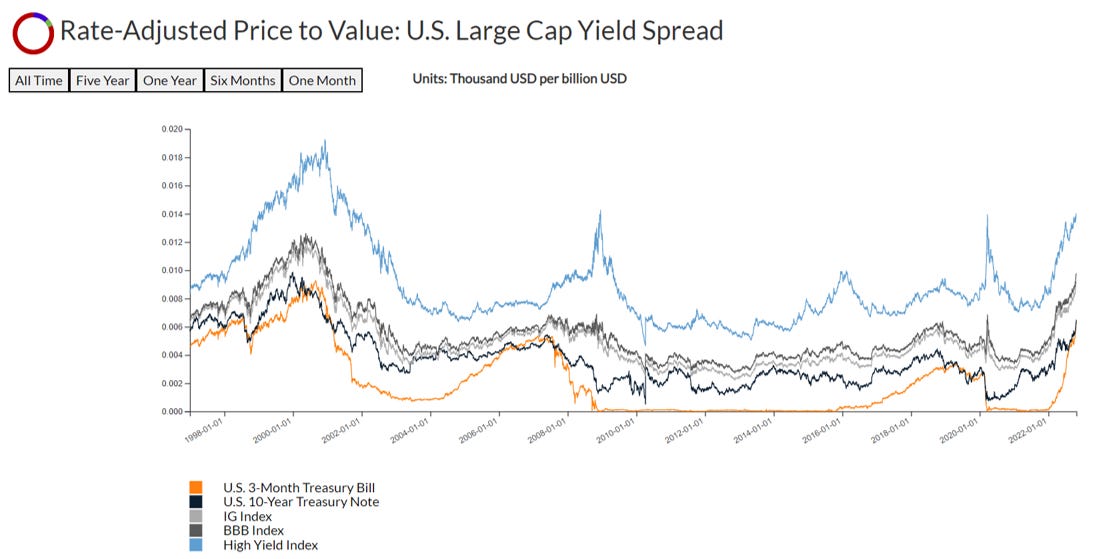

Yield Spreads: Corporate credit yields have risen significantly. IG and BBB debt now sit above their 2020 highs (mostly driven by increases in interest rates rather than credit spreads). HY debt sits just below its prior 2020 high. Notably the 3-month T-Bill and 10-year T-Note are now inverted (a harbinger for recession).

Yield-adjusted Price to GDP: Yield-adjusted Price to GDP has continued to rise. Notably, HY is at levels last seen in 2020 and IG and BBB both exceed levels seen in 2020.

10-Year to 3-Month Treasury Spread: The 10-year to 3-month treasury spread has now inverted (to -0.07 down from 0.34 in July 2022).

The 10-Year to 2-Year Treasury Spread is also deeply inverted (to a level last seen during the 2000 Dot-com bubble).

Notably, the divergence divergence between the 10-Year, 2-Year, 3-Month and Federal Funds Rate has closed significantly. Historically, the 3-month, 2-year Treasuries and Federal Funds rate invert prior to the end of a hiking cycle.

Inflation Break-Evens: Intermediate and long-run inflation averages remain stabilized ~2.5% (still well above the 2% long-run inflation target of the Federal Reserve). As mentioned earlier, some volatility will likely arise from this point on, as marginal changes in financial conditions affect expectations.

Housing Affordability:

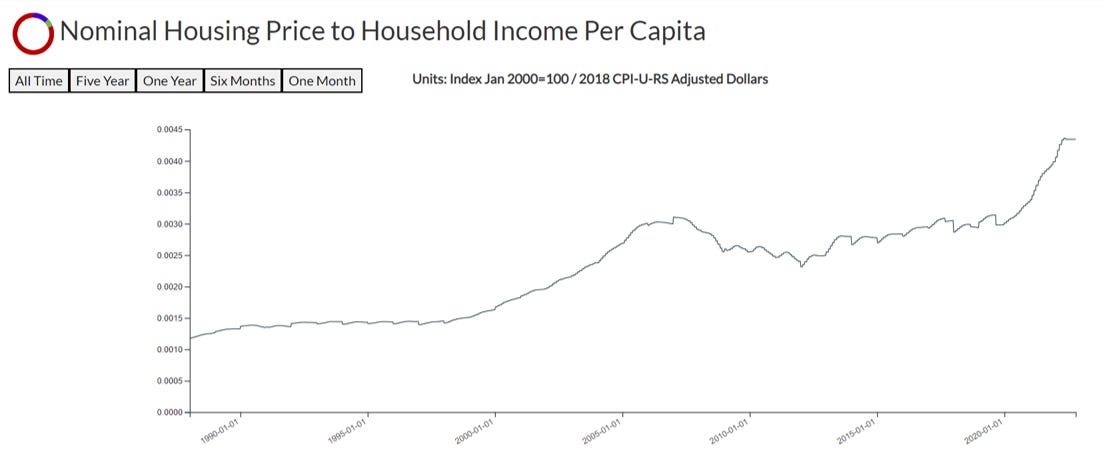

30-Year Mortgage-adjusted Housing Price to Household Income: The historic unaffordability in housing that began in Q1 has continued. Notably, an estimate of average mortgage payments to average household income has continued to increase well above circa 2006-2008 levels (largely on the back of a >7% mortgage rates).

Housing Price to Household Income: Housing affordability in absolute terms of housing price to household income continues to exceed levels last seen in the 2006-2008 housing/financial crisis. Notably, it appears to have begun to roll over (as last seen in the 2006-2008 episode).

Disclaimer

The data displayed in this report was developed by DeCotiis Analytics LLC (“DeCotiis Analytics”) using various public sources. DeCotiis Analytics is NOT a registered investment adviser and does not guarantee the accuracy or completeness of the information contained herein, or any data or methodology either included herein or upon which it is based. Individual investment decisions are best made with the help of a professional investment adviser.

Although effort has been taken to provide reliable, useful information in this report, DeCotiis Analytics does not guarantee that the information is accurate, current or suitable for any particular purpose. Data contained in this report are those of DeCotiis Analytics currently and are subject to change without notice. DeCotiis Analytics makes no guarantee or warranty of the accuracy of source data or the results of compilation of such data.

The information provided herein is for informational and educational purposes only. It should not be considered financial advice. You should consult with a financial professional or other qualified professional to determine what may be best for your individual needs. DeCotiis Analytics does not make any guarantee or other promise that any results may be obtained from using the content herein. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence. To the maximum extent permitted by law, DeCotiis Analytics disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations prove to be inaccurate, incomplete, unreliable or result in any investment or other losses. Content contained or made available herein is not intended to and does not constitute investment advice and your use of the information or materials contained is at your own risk.

Information from this report may be used with proper attribution. All original text, graphs and compilations of data contained in this document are copyrighted material attributed to DeCotiis Analytics. Any reproduction or other unauthorized use of material herein is strictly prohibited without the express written permission of DeCotiis Analytics.

Really good article Will!

Agree with the vast majority of what you wrote, my only quibble might be on the impact to the real economy. My intuition says that the real economy (at least as i define it in my own mind) actually ends up gaining a bunch with the deleveraging. Ill try to convert that intuition into reasoned arguments and post back when i have. Anyways, appreciate the thought provocation and the excellent summary of where we are, how we got here vs a few months ago and some of the likely forward impacts.